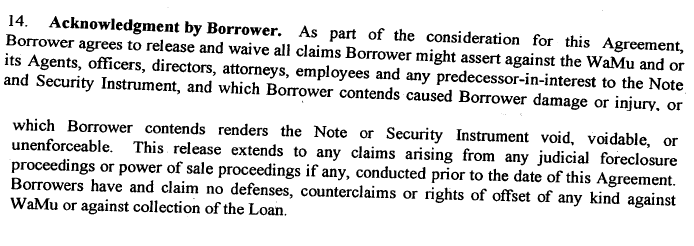

You can read his commentary as well as I can, so I won't recap, but if there was ever a doubt that those in charge (I'm talking about the Money Trust that owns congress) are wantonly accelerating the downturn to secure defaults and seize assets, then please take another look at the last page of his scanned WaMu loan modification:

[click to enlarge]

Such predatory modifications are aggressively endorsed and subsidized by our government. Our government will pay banks $1,000 for every loan modification agreement they can produce, plus 50% of the total loan default the bank is able to generate:

HR 7326

(a) In General- The Chairperson of the Federal Deposit Insurance Corporation shall establish a systematic foreclosure prevention and mortgage modification program by--

(1) paying servicers $1,000 to cover expenses for each loan modified according to the required standards; and

(2) sharing up to 50 percent of any losses incurred if a modified loan should subsequently re-default.

The "up to 50%" language means a full 50% as long as the loan principle is under the appraisal. There is no limit to the amount of interest and fees the government will reimburse the bank to impose. The bankers running Washington aren't only seizing the foreclosee's assets, they are seizing yours.

On a side note, it looks like the banks' lawyers were careless when they wrote the bill. I'd like to see homeowners claim the 50% provision, as it accidentally omits the word "servicer." The FDIC's charge is to pay injured people, not bankers.

So what are the mortgage refinancers trying to do exactly?

ReplyDeleteIt looks like a 5 year loan and at the end the entire principal of the house is due all at once? And they just take your house and sell half of it to the gov't if you don't pay up?

I am not following this exactly.

You're following this *exactly*.

ReplyDeleteThat is exactly what they're trying to do.

Hence, the word "predators" in the title...

Excellent post. Very informative. I think that if you just cannot pay, just give it up. The sooner, the better.

ReplyDeleteSo now they're paying for indemnification against future legal action, resulting from their previous criminal lending policies?

ReplyDeleteWell, most of these homeowners will end-up back in default in a few months anyway.

The scale of the fraud is staggering.

Why do they even bother to pretend any longer?

FDR, can you recommend any texts on the mechanics, structure, and operation of Central Banking, on both a national and international scale?

ReplyDelete(A text that could perhaps describe its inter-relationship and material workings on a daily basis with the BIS, IMF, Governments, Individual Taxation, and etc.)

the bad economic numbers are still driving s&p 500 high. impressively manipulation. the market is a three shell game. the host played it. all clients follow

ReplyDeleteDid I hear correctly that Muni bonds are going to be purchased under tarp. Does this mean that the govt is essentially backing muni paper that isn't insured? Would this move make muni bonds close to par with Tbills?

ReplyDelete"I am not following this exactly."

ReplyDeleteAs someone already said, you are following it EXACTLY. It boils down to this...

The government sponsored "solution" to the foreclosure problem is to pay banks $1,000 + half the total amount they can drown people farther underwater with increased mortgage balances, fees, and interest. Soon to be due in in one lump sum.

The (real) WaMu loan modification cited above adds $50,000 to the poor guy's bottom line, in exchange for lower payments for a few years, then it buries him dead by demanding over $1,000,000 payable IN FULL in five years, with perhaps, a $500,000 house to back it. Then the taxpayers pay what he cannot, the government gives the bank our money to kill the guy.

This is nothing but congress teaming up with banks to clobber her own citizens, so as to to massively increase bank profits, funded by the people.

How about the latest idea that will kill housing values completely. I forget the cute name the media calls it but it would allow judges to arbitrarily mark down the principal of a bankrupt person's home loan to what they can afford (or more accurately, what the judge THINKS the house value should be).

ReplyDeleteI get the part about helping the bankrupt people out, believe me, but when the activist judges start valuing houses at $10,000 just because they can, wow isn't this going to kill everybody's home values!

Good point, and as Bloomberg reported on Dec 18, the Federal "Hope Now" loan modification program had received 70 applications in its first month. So lets see...

ReplyDelete120,000,000 mortgages/10% in foreclosure or 90 days delinquent = 12,000,000 in need or already gone / 70 per month = 171,000 months

= 14,250 years

Gee, I wonder if we should try a market based solution instead of heavy handed government meddling? These people are 3rd grade math impaired.